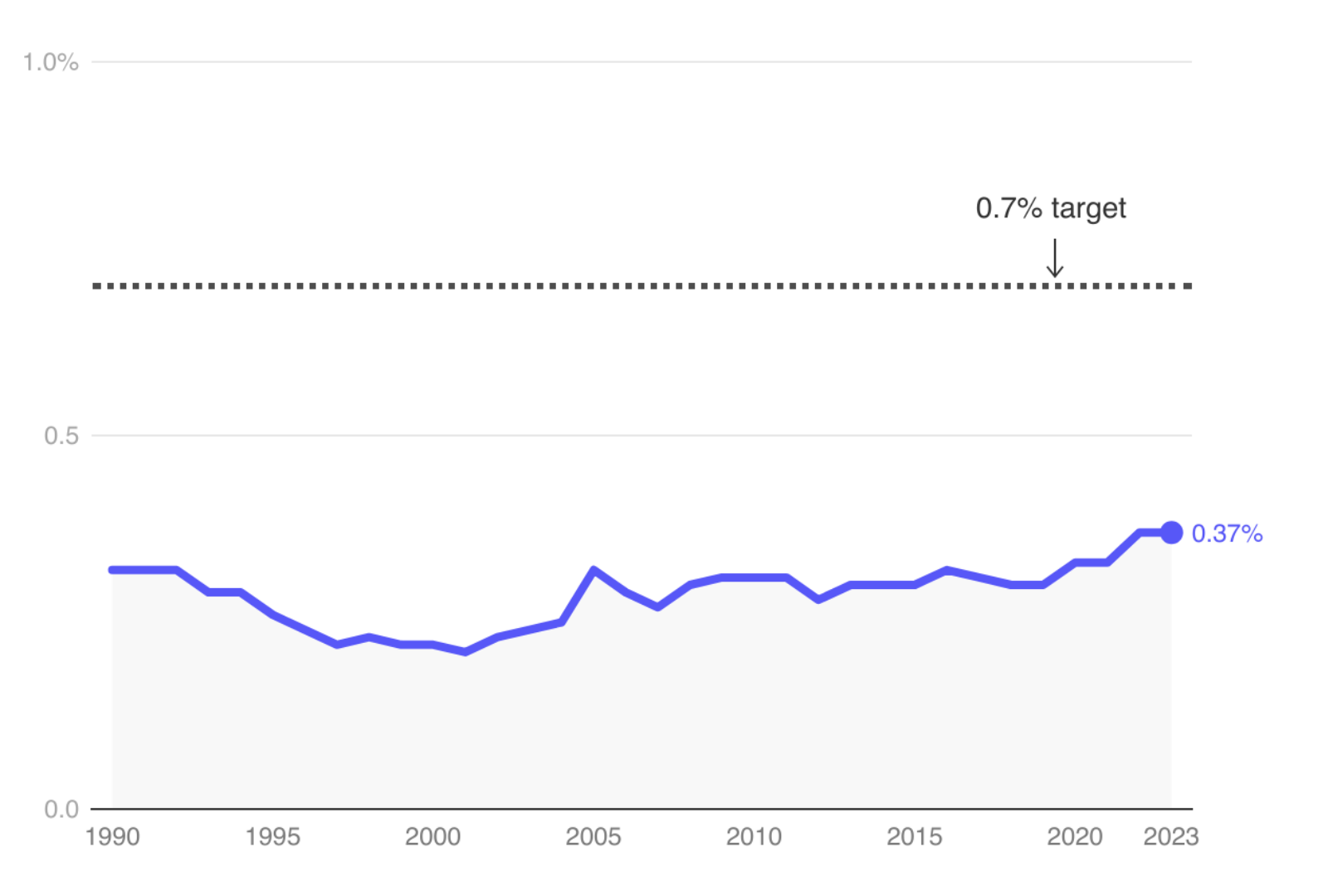

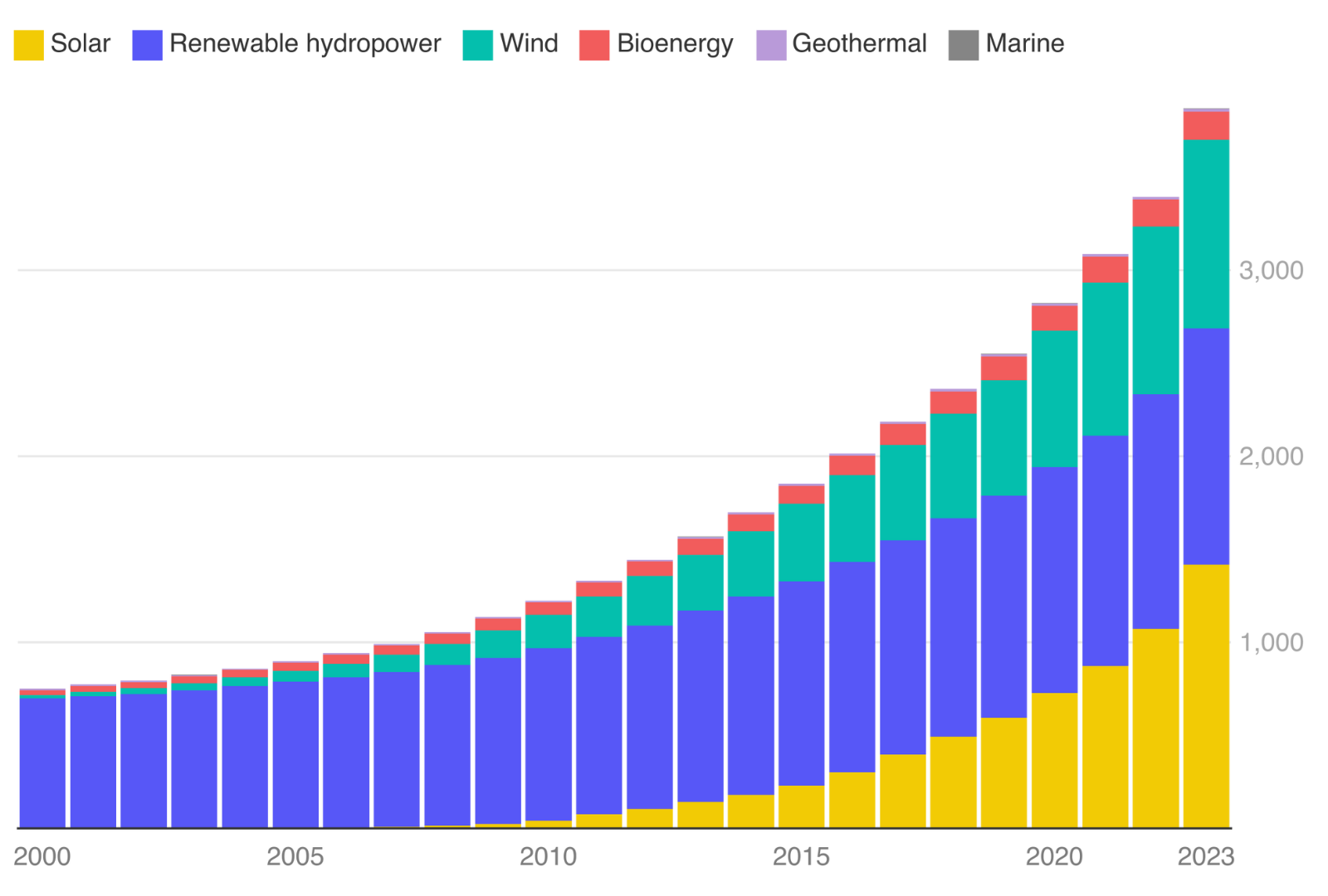

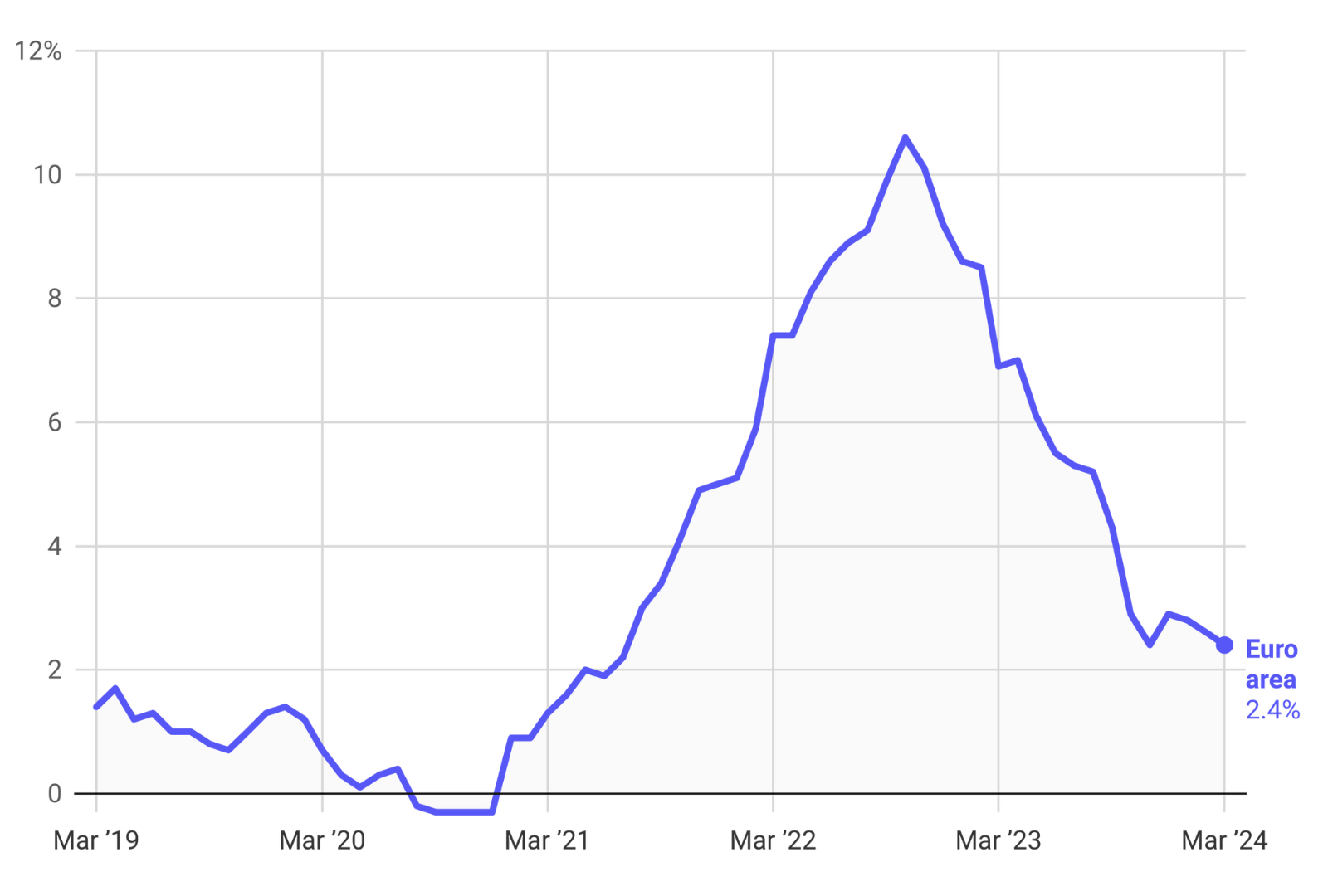

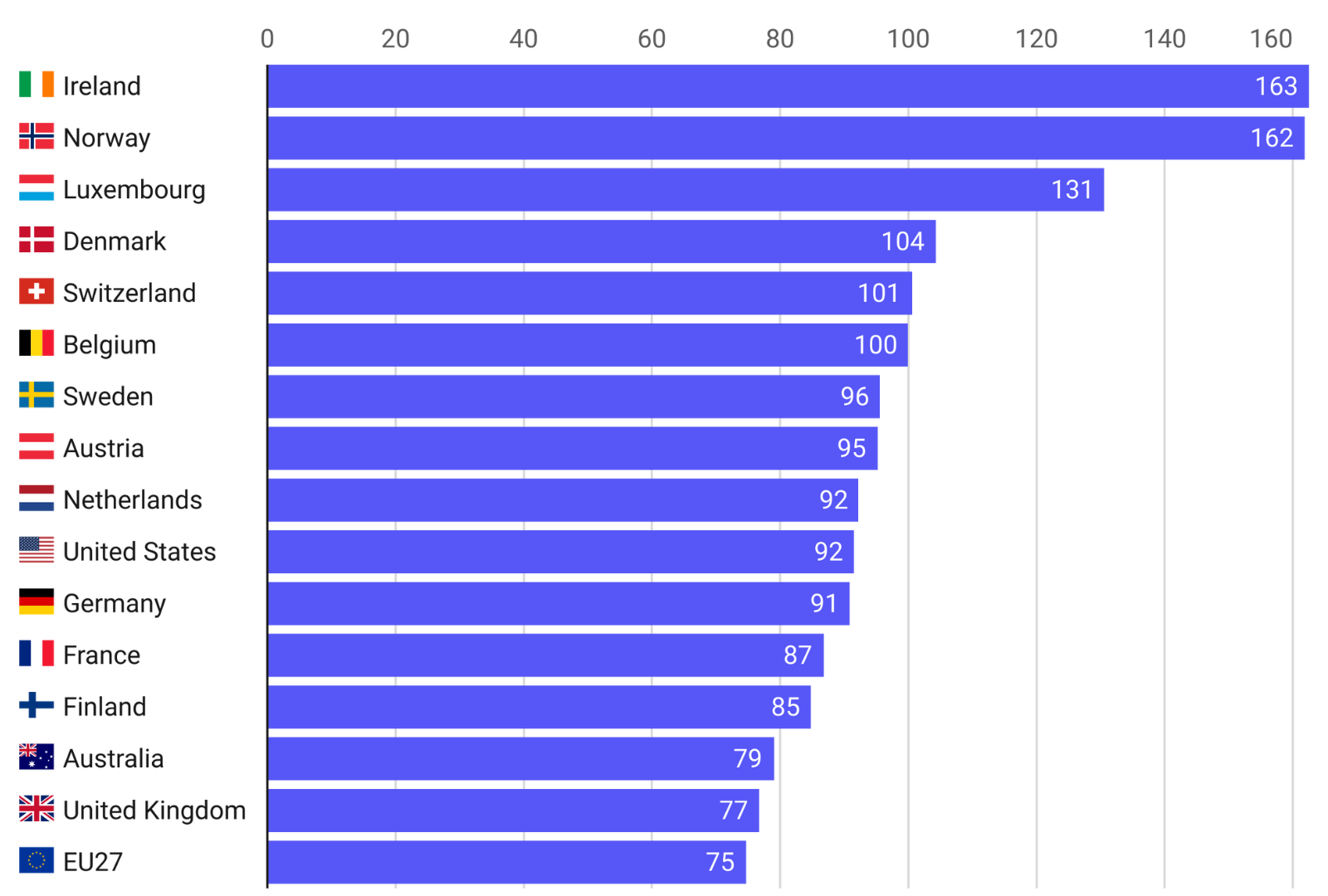

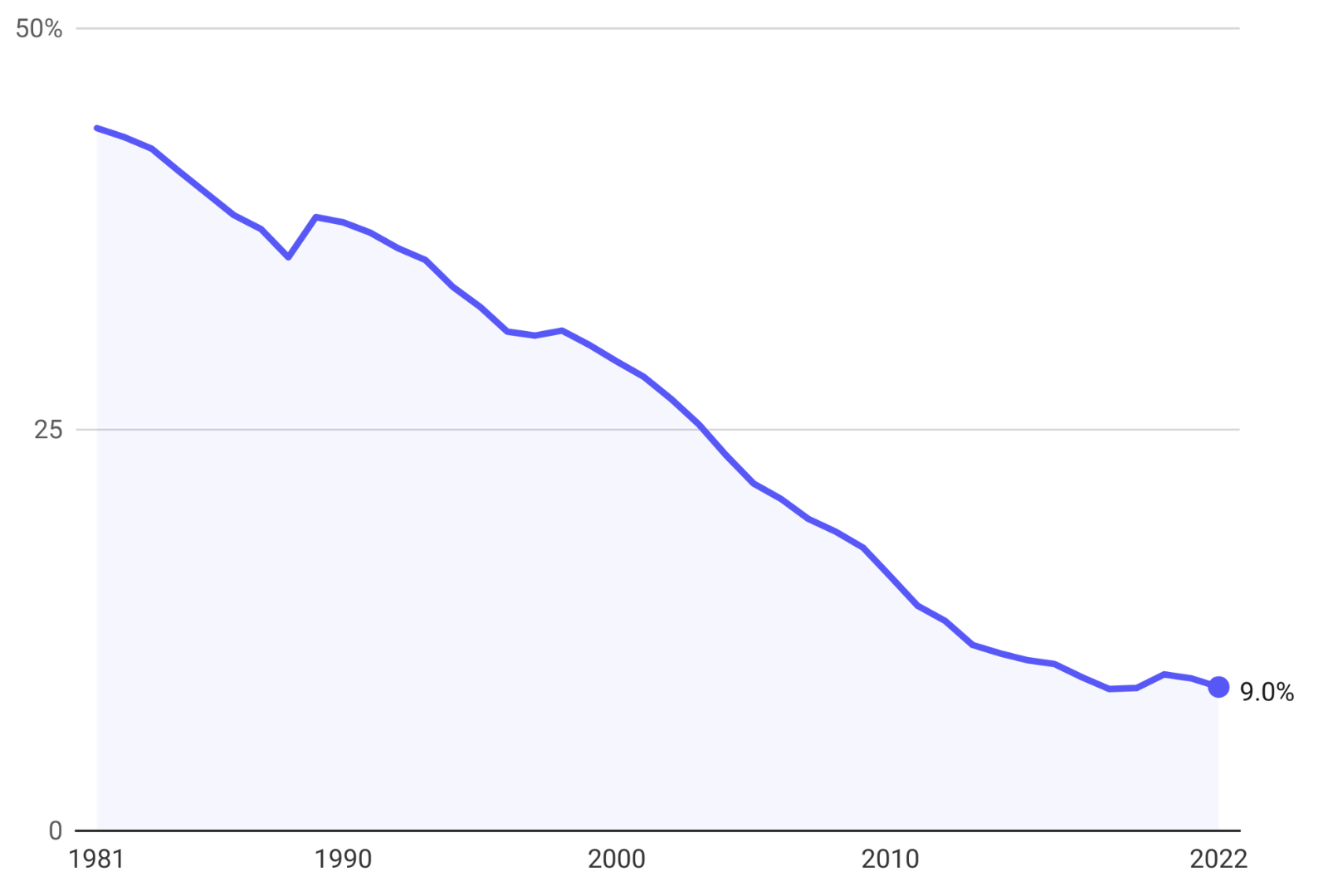

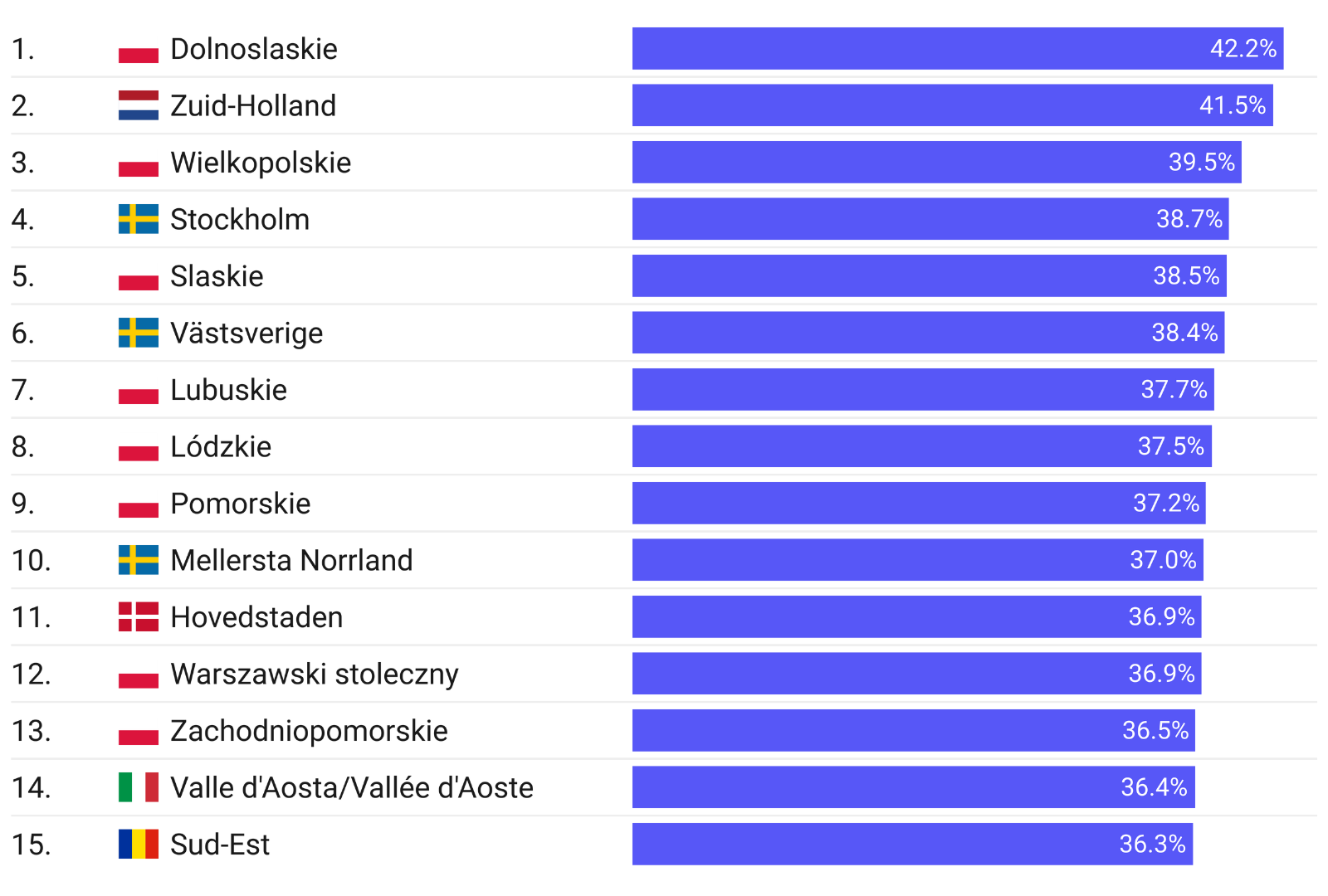

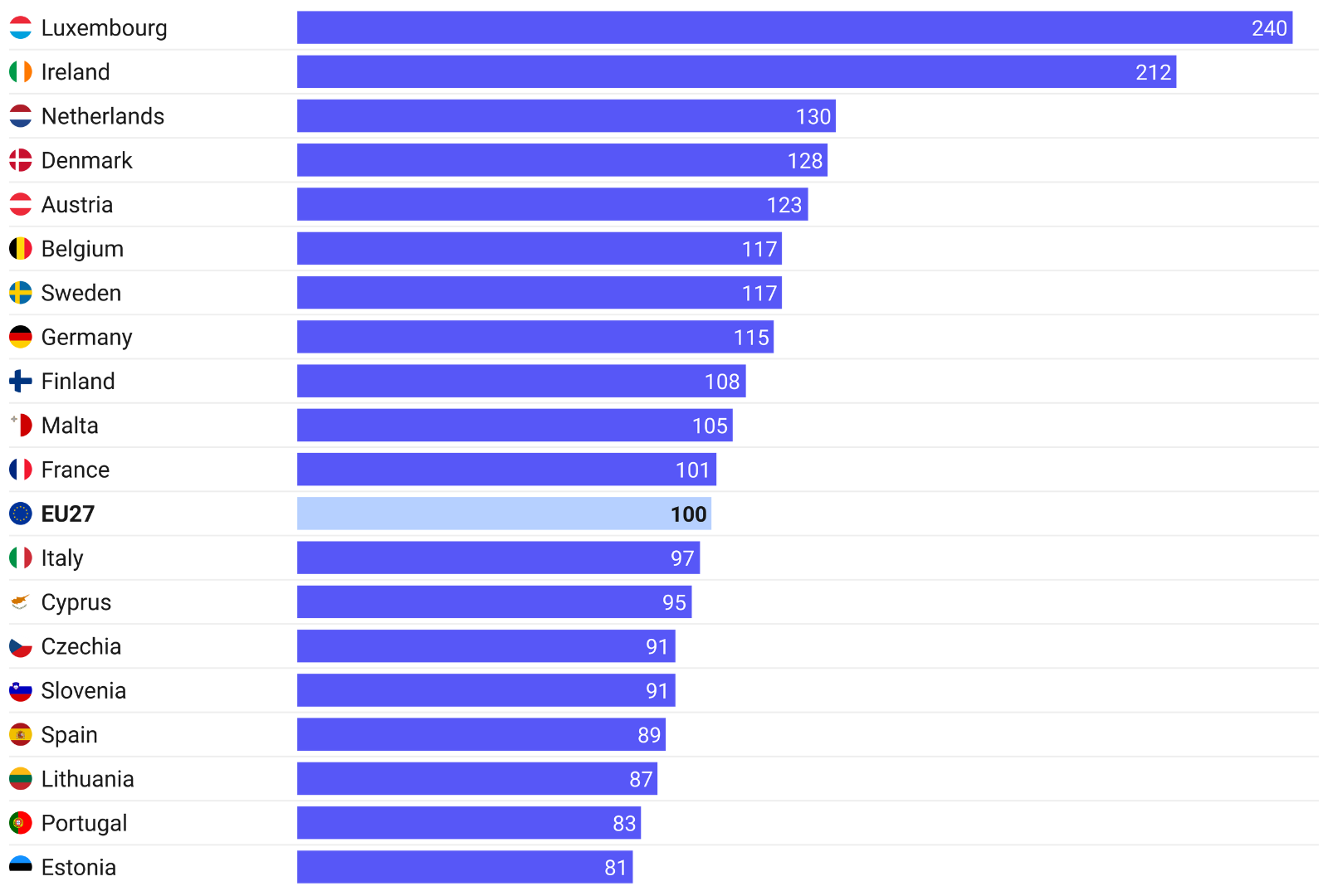

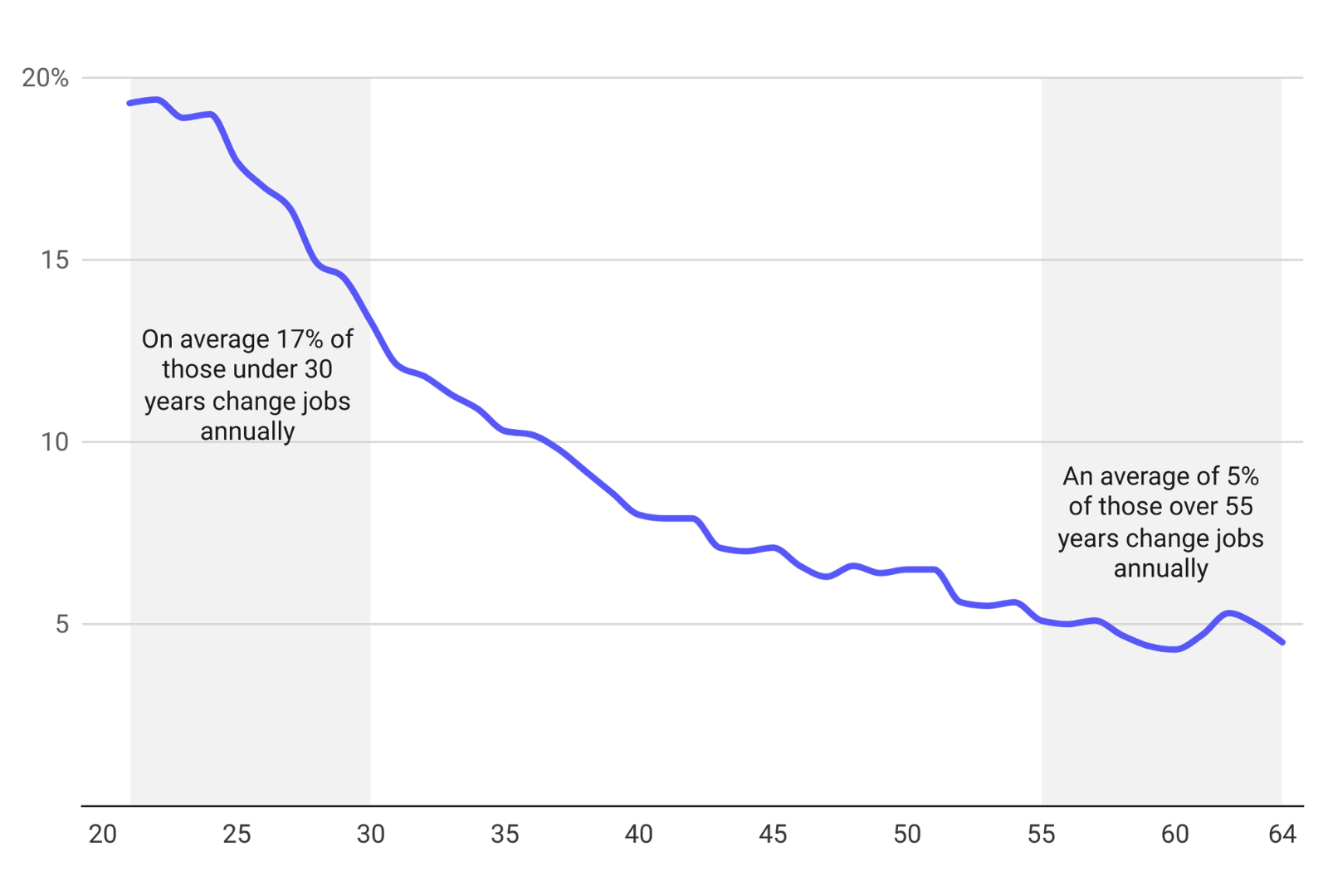

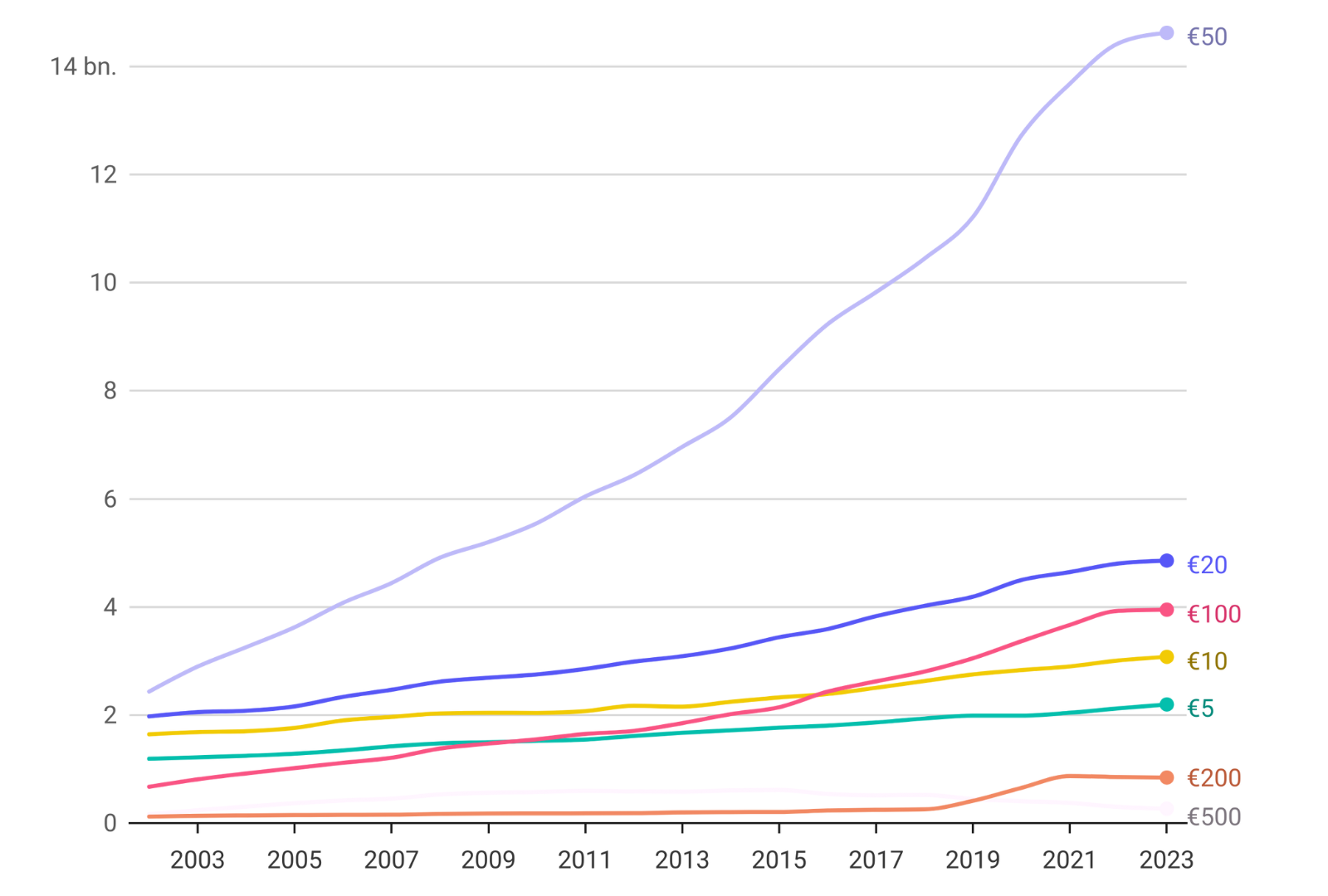

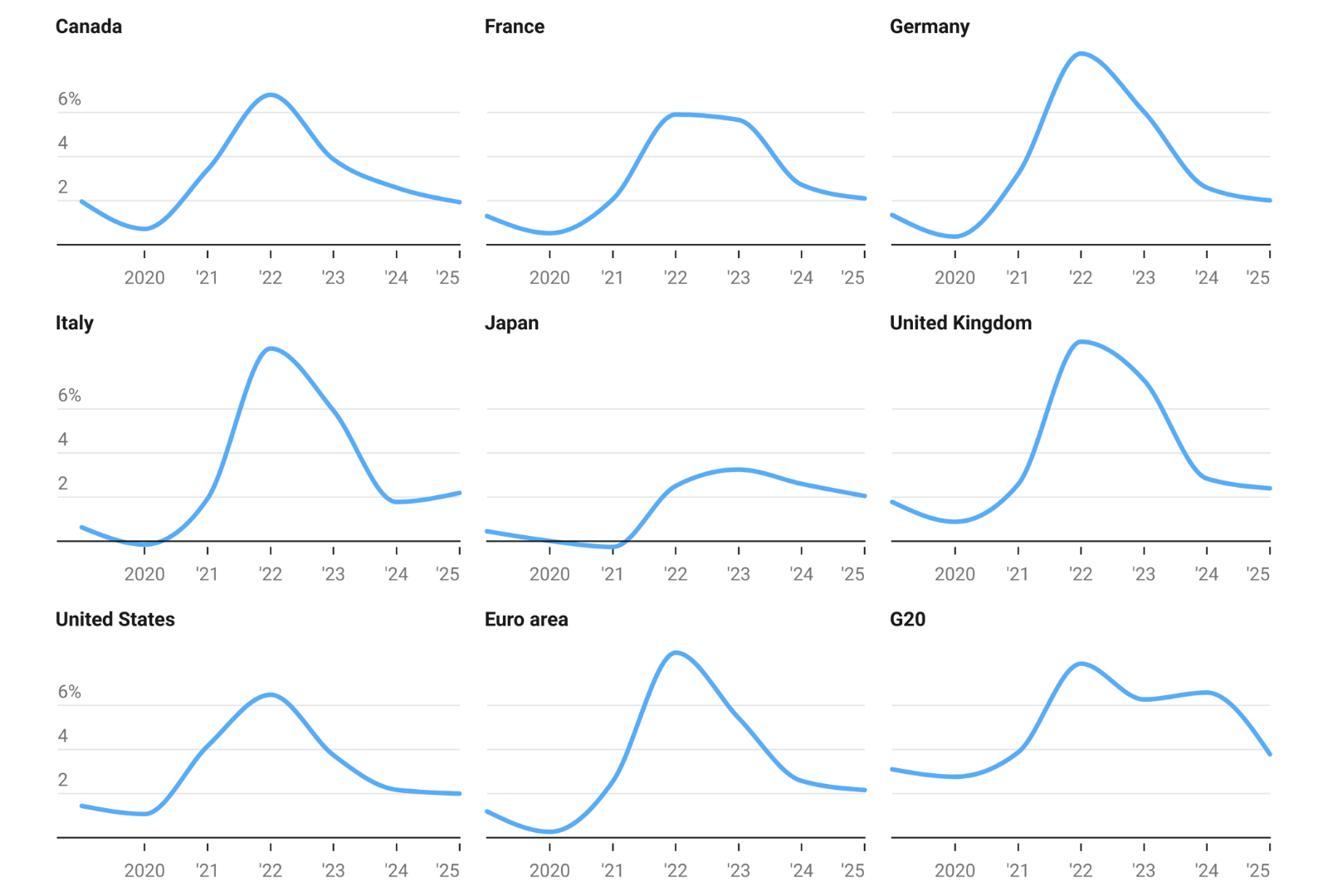

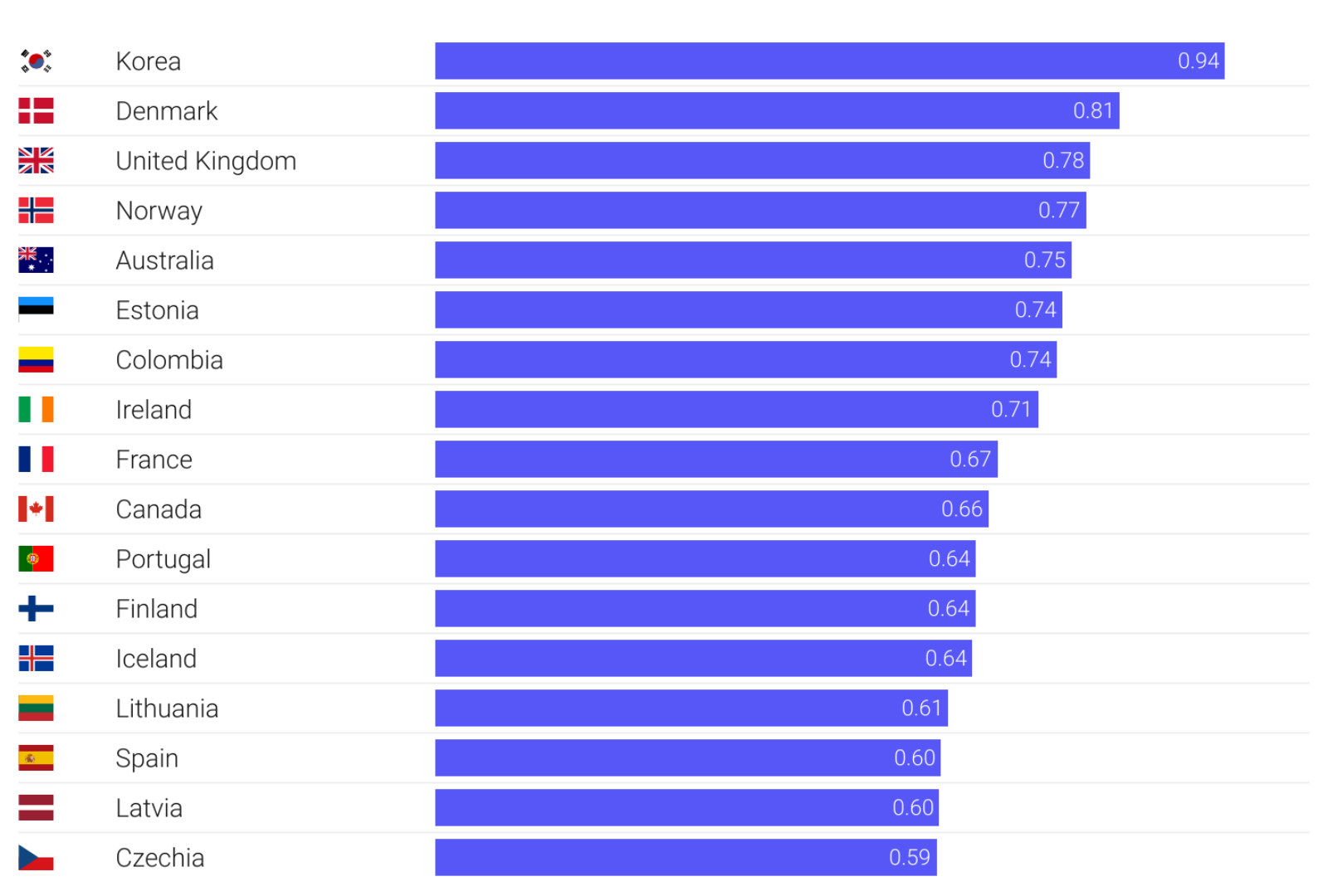

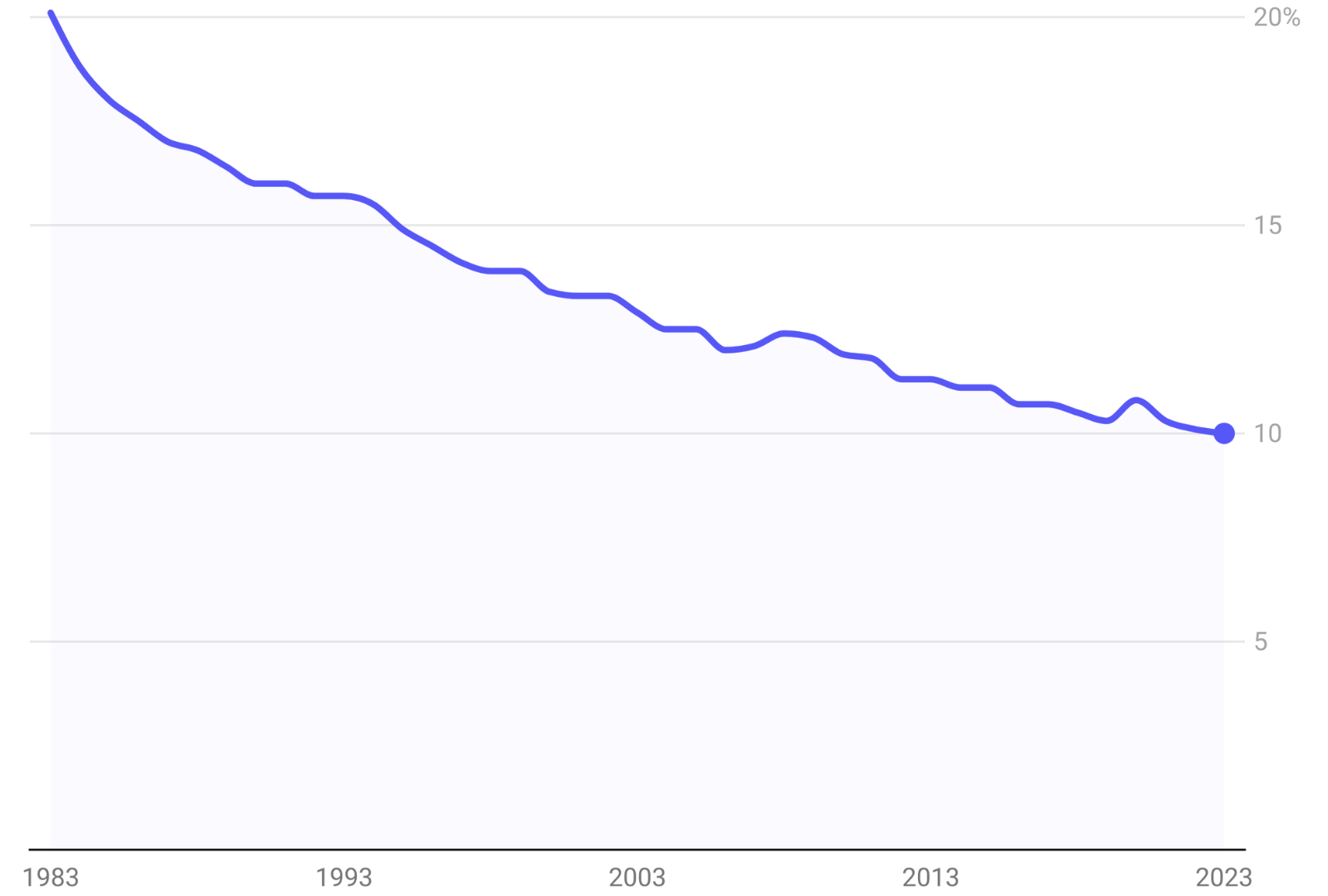

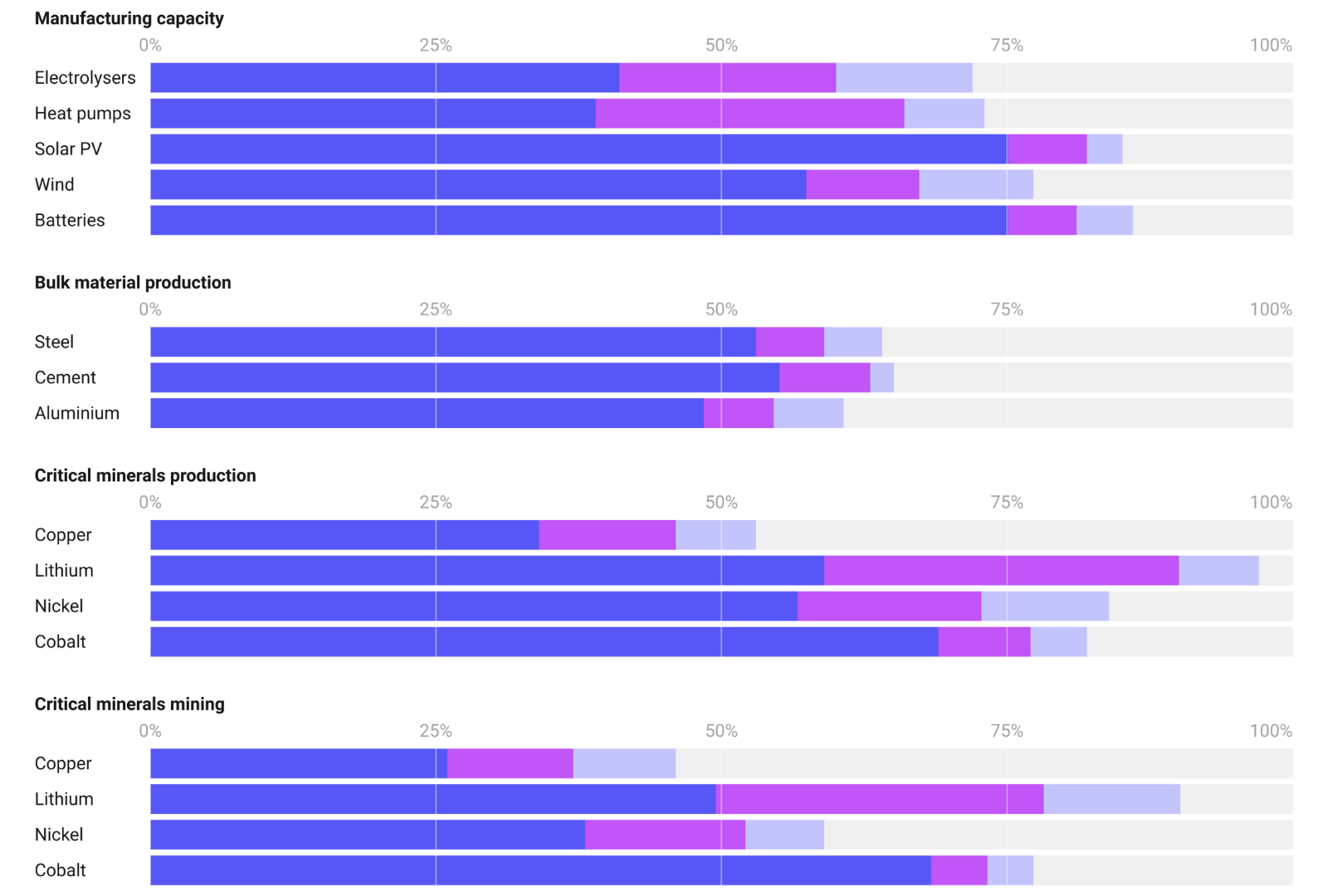

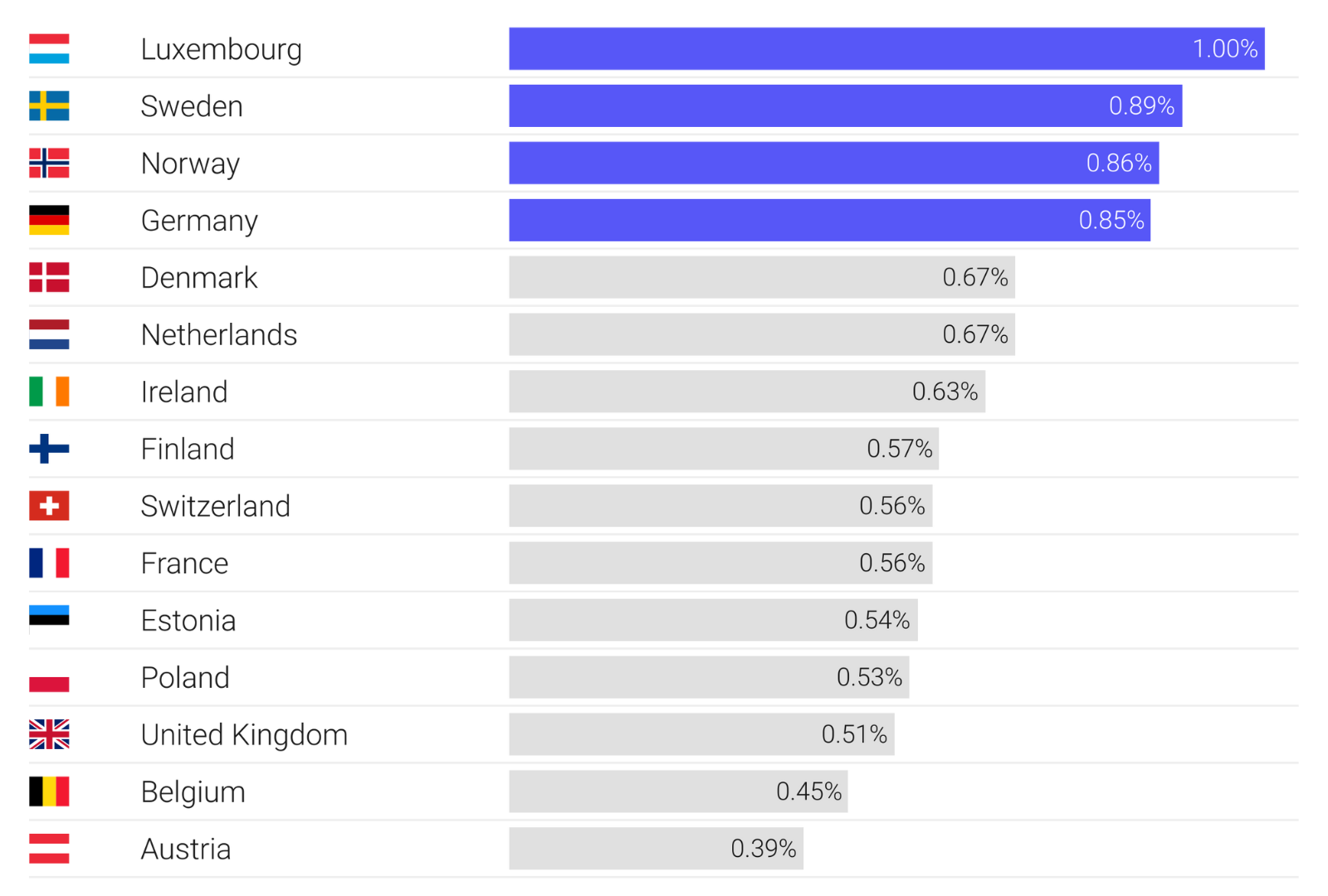

Data Spotlights Explore the latest posts on selected social and economic insights from across our socials: Instagram, Threads and Linkedin. Foreign Aid April 2024 Foreign Aid Increased to USD 224 bn in 2023, 0.37% of Donors Gross National Income Renewables April 2024 Renewable Energy Capacity Grew at Record Rate in 2023 Inflation April 2024 Euro Area Inflation Continues to Decline in March Productivity April 2024 Highest and Lowest Productivity Levels in OECD-countries in 2022 Poverty March 2024 712 Million People Living in Extreme Poverty, According to New World Bank Estimates Life Satisfaction March 2024 Public Opinion in EU Regions: Will Life Get Better, Worse or Stay the Same Over the Next Year? EU Economy March 2024 Wealth Differences in the EU: 2023 GDP per Capita Estimates Labour Markets March 2024 Job Mobility Declines with Age but Can Boost Wages and Employment Prospects Aviation March 2024 Air travel: 2023 Saw Lowest Fatality Risk and Accident Rate on Record Public Opinion March 2024 Eurobarometer Survey on Trust and Statistics Inflation March 2024 Eurozone Inflation Falls to 2.6% in February Climate Change March 2024 New 2023 Global Emissions Data Shows Shifting Regional Patterns Public Opinion March 2024 Public Opinion on National Direction: Right Track or Wrong Track? EU Regions February 2024 European Regional GDP in 2022 US Census February 2024 U.S. Census Household Pulse Survey Jan-Feb 2024 Labour Markets February 2024 The Growing Importance of Older Workers in the Workforce Life Satisfaction February 2024 How Does Life Satisfaction Vary by Income? Climate Change February 2024 Decoupling Emissions and Growth in the EU Inflation February 2024 EU Inflation Expected to Ease in 2024 and 2025 Security February 2024 NATO Europe Defense Expenditure Set to Reach 2% Labour Markets February 2024 Minimum Wage Levels in the EU 2024 Oil February 2024 Russian Oil Exports Pivots Towards the East Trade February 2024 U.S. Trade Deficit Narrows in 2023 Climate Change February 2024 Europe’s Climate Pathway After New 2040 Target Recommendation European Economy February 2024 How Do Europeans Judge the Current Situation in Their National Economy? Euro February 2024 Show Me the €: The Number of Euro Banknotes Circulating Inflation February 2024 Economic Forecast: OECD Sees Inflation Moving Back to Target Digitalisation February 2024 How Ready Are Governments for the Digital Transformation of Public Services? World Economy February 2024 IMF Raises 2024 Global Growth Forecast Trade Unions February 2024 Union Membership at Four Decade Low in the U.S. Renewable Energy January 2024 The Geographic Concentration of Clean Energy Supply Chains Foreign Aid January 2024 Only Four Countries Hit UN 0.7% Foreign Aid Target in 2022 1234